New Zealand Institute of Economic Research (Inc)

Media release

For release 10 am Monday, 23 May 2022

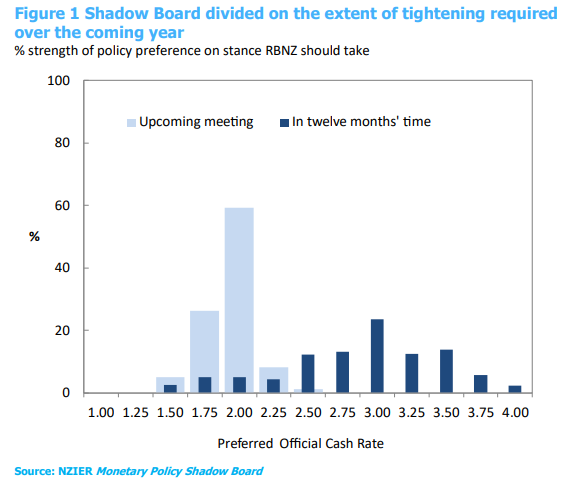

There is a wide range of views within the Shadow Board over how much the Reserve Bank should increase interest rates, particularly for the coming year. The majority view amongst Shadow Board members was that the Official Cash Rate (OCR) should be increased by 50 basis points at the May meeting. However, there was a divergence in views on how much the OCR should be increased beyond the May meeting. This wide range of views reflects both different concerns held by the Shadow Board members compounded by the large degree of uncertainty over the economic outlook over the coming year.

Inflation pressures are very strong both here in New Zealand and abroad. The COVID-19 outbreaks disrupted supply chains worldwide and led to a substantial rise in costs. The surge in inflation raises the risk of longer-term inflation expectations becoming unanchored, and central banks around the world have started tightening monetary policy to rein in inflation pressures. However, the war in Ukraine and lingering uncertainty over how the COVID-19 outbreaks and higher interest rates will affect demand have led some Shadow Board members to be more cautious about the extent of interest rate increases over the coming year.

Table 1 Participant comments

Participant comments are optional

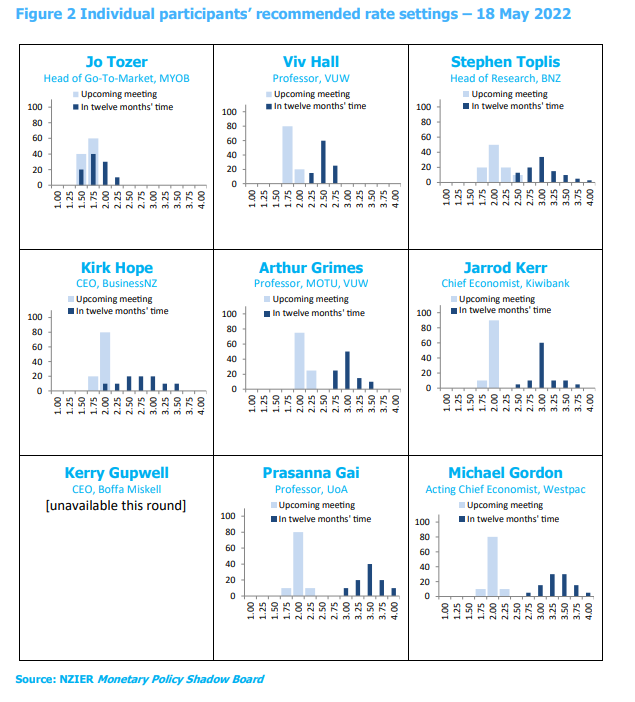

| Stephen Toplis | There is little doubt rates need to head above neutral. The debate is how much and how fast. The outcome will be the winner in the tug of war between ongoing capacity constraints and recessionary possibilities. This means there is a widespread of potentially appropriate rates for twelve months; hence, 3.0% is our centre point within this spread. |

| Viv Hall | Core inflationary pressures continue stronger than desirable, and RBNZ two-year inflationary expectations remain elevated at 3.3%. An immediate 25 bp increase in the OCR is required. The case for another 50 bp increase is not clear cut. Global economic activity has slowed somewhat, global monetary policy has belatedly begun to tighten, and there is some initial traction from New Zealand's recent OCR increases. |

| Kirk Hope | No comment. |

| Jarrod Kerr | The “stitch in time” approach should see another 50bp move in May to 2%. 2% is deemed to be neutral, and therefore no longer stimulatory. We expect to see a peak in this cycle around 3%. Rapidly rising interest rates are having an impact. 70% of the total Kiwi mortgage book is rolling off lower rates and onto much higher rates this year. Discretionary spending will be reduced, and confidence surveys are already reflecting the stresses on household and business balance sheets. |

| Jo Tozer | In the latest MYOB Budget Snapshot, 74% of SMEs were extremely concerned or quite concerned about current inflation levels, while over half (56%) thought the Reserve Bank isn’t currently doing enough to help manage inflation. So while rising interest rates will increase their finance costs, SMEs are likely to accept that additional rate rises may be necessary to curb the immediate threat of further inflation. |

| Arthur Grimes | No comment. |

| Michael Gordon | Reining in domestic inflation pressures will take some time. The process is underway, but the RBNZ will need to follow through with the OCR hikes that have been signalled. |

| Prasanna Gai | No comment. |

About the NZIER Monetary Policy Shadow Board

NZIER’s Monetary Policy Shadow Board is independent of the Reserve Bank of New Zealand. Individuals’ views are their own, not those of their respective organisations. The next Shadow Board release will be Monday, 11 July 2022, ahead of the RBNZ’s Monetary Policy Review. Past releases are available from the NZIER website: www.nzier.org.nz

Shadow Board participants put a percentage preference on each policy action. Combined, the average of these preferences forms a Shadow Board view ahead of each monetary policy decision.

The NZIER Monetary Policy Shadow Board aims to:

- encourage informed debate on each interest rate decision

- help inform how a Board structure might operate

- explore how Board members could use probabilities to express uncertainty.

Christina Leung, Principal Economist & Head of Membership Services

christina.leung@nzier.org.nz, 021 992 985

Share this

Shadow Board members recommend the Reserve Bank gets on with OCR increases

Shadow Board is divided over whether the Reserve Bank should increase the OCR in May