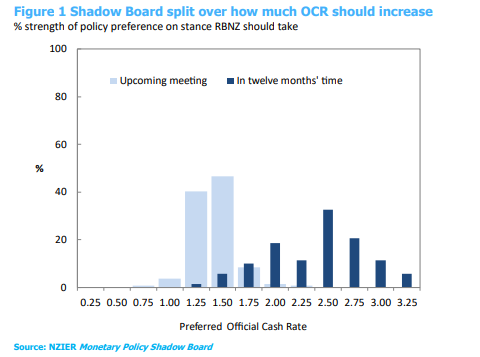

The Shadow Board is sharply divided over how much the Reserve Bank should increase the Official Cash Rate (OCR) at the April meeting, with views split over whether the OCR should increase by 25 or 50 basis points. The surge in inflation pressures has led to growing calls for the Reserve Bank to undertake monetary policy tightening at a more aggressive pace to rein in these inflation pressures. While supply-side constraints are driving much of the increase in inflation in the New Zealand economy, the recent rise in longer-term inflation expectations raises the risk of a wage-price spiral developing.

However, some Shadow Board members called for caution in the pace of interest rate increases over the coming year. The recent weakening in business and consumer confidence due to uncertainty stemming from the spread of the more transmissible Omicron variant of COVID-19 and the war in Ukraine were provided as reasons for a more measured pace of monetary tightening.

Beyond the April meeting, there is a wide range of views amongst the Shadow Board on where the OCR should end up in twelve months’ time. Shadow Board members highlighted the balance between the need to rein in inflation pressures against the extent to which the New Zealand economy will slow in response to interest rates increases and the heightened uncertainty over the global growth outlook.

Table 1 Participant comments

Participant comments are optional.

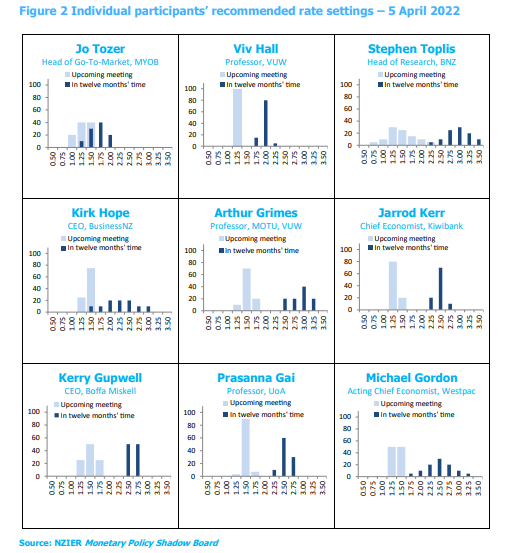

| Stephen Toplis | There is no doubt the cash rate needs to rise and keep rising until it is through neutral. The only point of contention is how fast and how far. |

| Viv Hall | After taking due account of supply side and 'look through' factors, demand side inflationary pressures and higher inflationary expectations will continue to predominate for some time yet. A further immediate 25bp increase in the OCR is therefore necessary. Subsequent increases should be evaluated as the relative strengths of demand, inflationary expectations and other factors evolve. |

| Kirk Hope | No comment. |

| Jarrod Kerr | I don’t believe the RBNZ needs to deliver 50bp moves. Business and consumer confidence has been pulled down by the Omicron outbreak and rising commodity prices with the war in Ukraine. Sufficient monetary tightening is coming through bank lending rates in anticipation of RBNZ moves |

| Jo Tozer | MYOB’s 2022 Business Monitor shows the rate of inflation is currently the second largest local factor (after COVID-19) impacting economic confidence of SMEs (55%). Economic confidence has also reached its lowest level since the start of the pandemic. As a result, RBNZ's monetary policy (next 12 months) should target growing inflationary pressures which could increase the cost of goods, push up wage costs, and constrain consumer demand. |

| Kerry Gupwell | While house prices are easing, upward pressures on inflation seem to be intensifying suggesting inflation is “stickier” than some have suggested. Supply chain issues, full employment, Omicron impacts, government monetary policy all seem to point to higher inflation. There needs to be another increase in the OCR of 50 basis points. |

| Arthur Grimes | When a central bank is so far behind the curve as the RBNZ is, it needs to tighten aggressively. |

| Michael Gordon | Falling house prices show that the RBNZ is getting the traction that it needs to bring down domestic inflation pressures. To ensure success, it will need to follow through and deliver the cumulative rate hikes that the market has factored in, although that on its own doesn’t resolve the question around tactics from meeting to meeting. |

| Prasanna Gai | No comment. |

About the NZIER Monetary Policy Shadow Board

NZIER’s Monetary Policy Shadow Board is independent of the Reserve Bank of New Zealand. Individuals’ views are their own, not those of their respective organisations. The next Shadow Board release will be Monday, 23 May 2022, ahead of the RBNZ’s Monetary Policy Statement. Past releases are available from the NZIER website: www.nzier.org.nz

Shadow Board participants put a percentage preference on each policy action. Combined, the average of these preferences forms a Shadow Board view ahead of each monetary policy decision.

The NZIER Monetary Policy Shadow Board aims to:

- encourage informed debate on each interest rate decision

- help inform how a Board structure might operate

- explore how Board members could use probabilities to express uncertainty.

Christina Leung, Principal Economist & Head of Membership Services

christina.leung@nzier.org.nz, 021 992 985

Share this

Shadow Board is divided over whether the Reserve Bank should increase the OCR in May

Shadow Board recommends the Reserve Bank hikes the OCR by 50 basis points in August and follow up with further tightening