New Zealand Institute of Economic Research (Inc)

Media release

For release 10 am Monday, 3 October 2022

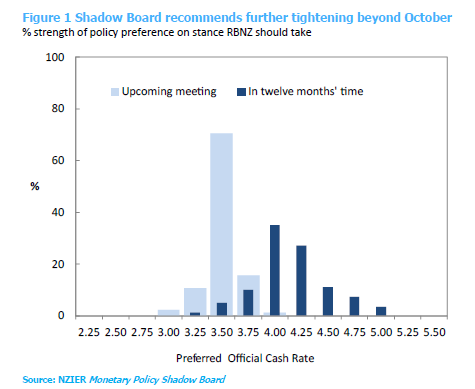

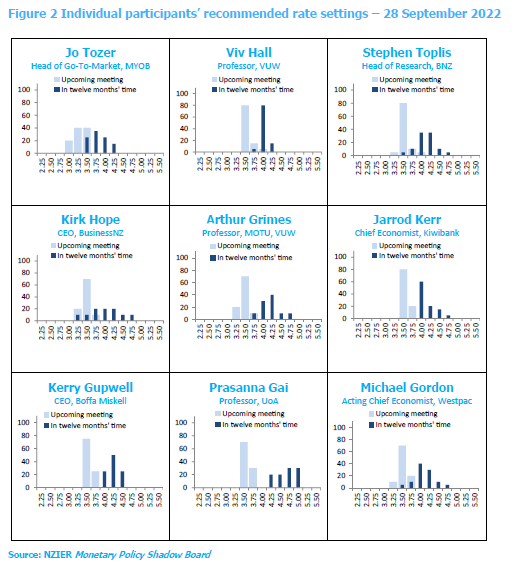

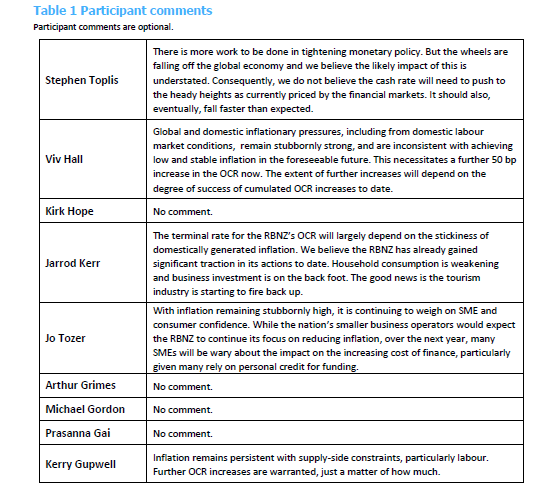

The broad view amongst the Shadow Board is that the Reserve Bank of New Zealand should raise the official cash rate (OCR) by another 50 basis points to 3.50 percent at the upcoming October meeting. Only one member does not recommend such a large increase due to concerns about business and consumer confidence and the increasing cost of finance. Shadow Board members highlighted that domestic constraints, particularly labour, are keeping inflation high.

The Shadow Board’s core view regarding where the OCR should be in a year ranged from 3.50 percent to 4.75 percent. Inflation is still the main concern for the New Zealand economy, and further monetary tightening was considered necessary. However, there was a range of views on the degree of further tightening. One Shadow Board member noted the risks of a hard landing in the global economy and the potential impact of this on New Zealand. Another member was concerned with the increasing cost of finance for small businesses if interest rates rise further. Some Shadow Board members highlighted that the extent of further OCR increases depends on how domestically generated inflation responds to the cumulative changes in the OCR to date. With demand from household consumption and business investment weakening, the economy is showing signs of RBNZ’s monetary tightening, gradually achieving its intended effect.

About the NZIER Monetary Policy Shadow Board

NZIER’s Monetary Policy Shadow Board is independent of the Reserve Bank of New Zealand. Individuals’ views are their own, not those of their respective organisations. The next Shadow Board release will be Monday, 21 November 2022, ahead of the RBNZ’s Monetary Policy Review. Past releases are available from the NZIER website: www.nzier.org.nz

Shadow Board participants put a percentage preference on each policy action. Combined, the average of these preferences forms a Shadow Board view ahead of each monetary policy decision.

The NZIER Monetary Policy Shadow Board aims to:

- encourage informed debate on each interest rate decision

- help inform how a Board structure might operate

- explore how Board members could use probabilities to express uncertainty.

Ting Huang, Senior Economist

ting.huang@nzier.org.nz, 027 266 0969

Share this

Shadow Board is divided over a 25 or 50 basis-point cut in the OCR in October

Shadow Board is divided over whether the RBNZ should hike by 50bp