New Zealand Institute of Economic Research (Inc)

Media release

For release 10 am Monday, 22 May 2023

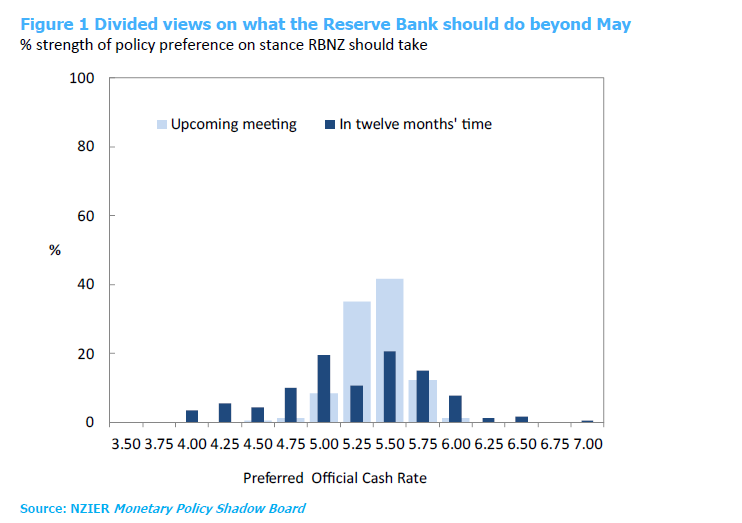

The Shadow Board is divided over whether the Reserve Bank should increase the Official Cash Rate (OCR) in the May Monetary Policy Statement. A larger number of Shadow Board members viewed an OCR increase of 25 basis points to 5.50 percent is warranted, given domestic inflation pressures remain high and the upside risk to inflation due to the weather events earlier this year. The rest of the Shadow Board members recommend the Reserve Bank should keep the OCR at 5.25 percent. One member highlighted that household inflation expectations are already heading in the right direction, and monetary policy takes time to have an impact. One was also concerned about the continued decline in profitability for businesses as consumers are increasingly more cautious about spending.

There was a divergence in views amongst the Shadow Board on where the OCR should be in twelve months. They reflect the different concerns held by the Shadow Board members about the economic outlook for the coming year. Recent developments, such as weaker Government tax revenue and consumer spending, and continued declines in business profitability, point to a slowing in the New Zealand economy. Two members also pointed out the potential upside risk to inflation from rising net migration inflows and any new fiscal stimulus in the new Budget, which the Reserve Bank should keep their eyes on.

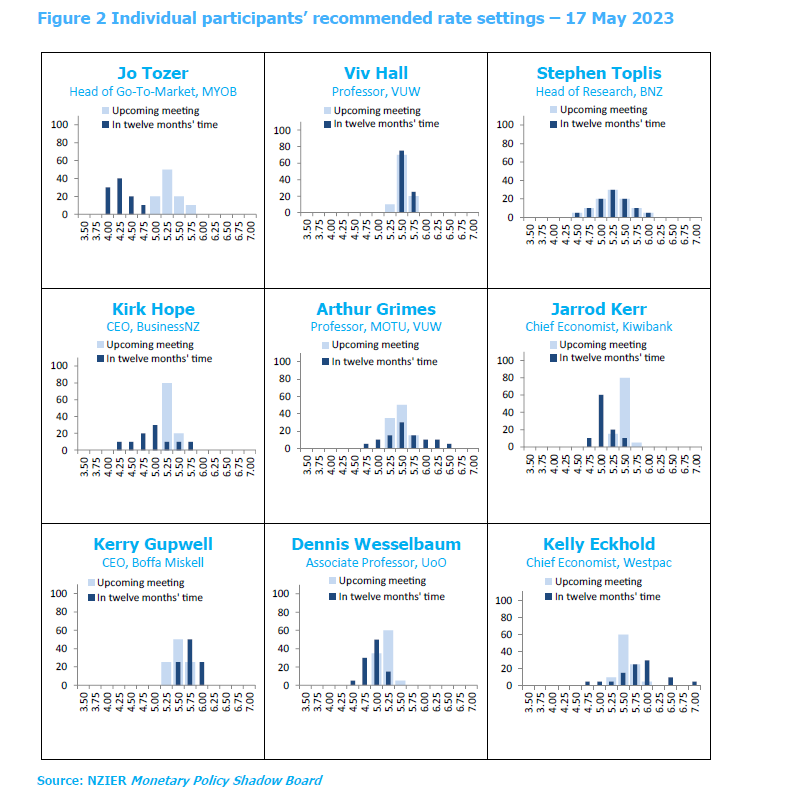

Table 1 Particpants' comments

Participant comments are optional

| Stephen Toplis | As we approach a turning point, the margin for error grows. The relative supply/demand impact of migration is a huge uncertainty and could well be the key determining factor for the next year or so. Keep an eye on the state of fiscal stimulus too. |

| Viv Hall | No comment. |

| Kirk Hope | No comment. |

| Jarrod Kerr | The Kiwi economy has turned sharply over the last 6 months. Government revenues, through corporate tax and GST, are coming in below forecast. The downshift in the Govt’s coffers confirms the downshift in spending on Kiwibank credit and debit cards. Household consumption has cooled, and looks to be contracting. The recession the RBNZ says we have to have is upon us. |

| Jo Tozer | Rising costs and cautious consumer spending are hitting businesses hard. MYOB’s 2023 Business Monitor reveals 45% of SMEs saw their profitability decline in the last three months and revenue for the past 12 months is down for 1/3 of local operators. Over a third of the SMEs concerned about the impact of rising interest rates on their business finances, said they’d need to dip into their personal finances for their business if interest rate increases continue. |

| Arthur Grimes | No comment. |

| Kelly Eckhold | No comment. |

| Kerry Gupwell | While overall inflation seems to have peaked, domestic (non-tradable) inflation remains a concern and cyclone Gabrielle hasn’t helped. It will be interesting to see what the May budget reveals as well – especially in an election year. On balance, I think another 25 basis points increase in the OCR is warranted, although there are signs that companies and households are starting to tighten their belts. |

| Dennis Wesselbaum | PPI and CPI are falling, mortgage repayment liabilities are increasing, jobseeker support is up, and so is hardship assistance. CPI is still outside the target range, but median household inflation expectations are moving in the right direction. Given the lags of monetary policy, I would stop increasing the OCR. |

About the NZIER Monetary Policy Shadow Board

NZIER’s Monetary Policy Shadow Board is independent of the Reserve Bank of New Zealand. Individuals’ views are their own, not those of their respective organisations. The next Shadow Board release will be Monday, 10 July 2023, ahead of the RBNZ’s Monetary Policy Review Past releases are available from the NZIER website: www.nzier.org.nz

Shadow Board participants put a percentage preference on each policy action. Combined, the average of these preferences forms a Shadow Board view ahead of each monetary policy decision. The results are not a prediction of RBNZ’s behaviour. They reflect the Shadow Board’s view on the appropriate setting of OCR given the current economic settings.

The NZIER Monetary Policy Shadow Board aims to:

- encourage informed debate on each interest rate decision

- help inform how a Board structure might operate

- explore how Board members could use probabilities to express uncertainty.

Ting Huang, Senior Economist

ting.huang@nzier.org.nz, 027 266 0969

Share this

Shadow Board is divided over whether the Reserve Bank should ease the OCR in August

Shadow Board is divided over whether the RBNZ should hike by 50bp