New Zealand Institute of Economic Research (Inc)

Media Release, 10 am Monday, 6 July 2026

For immediate release

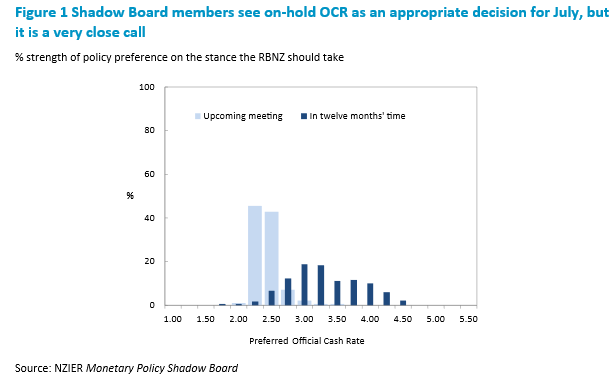

There is a split of views amongst the NZIER Monetary Policy Shadow Board regarding the Official Cash Rate (OCR) at the upcoming July Monetary Policy Review. Shadow Board members, on balance of strength of view, recommend the Reserve Bank of New Zealand (RBNZ) keep the OCR unchanged at 2.25 percent in July. However, it has become a line-ball call in terms of whether the RBNZ should keep the OCR on hold or raise it by 25 basis points in the July meeting. Rising inflation was a key reason given by members who want the OCR moved back towards neutral sooner rather than later. There was a range of views on the effect of the oil price shock on inflation and the New Zealand economy over the next year.

Regarding where the OCR should be in a year, Shadow Board members continue to agree that the RBNZ should increase the OCR over the coming year. Views on where the OCR should be in a year’s time centred around 3 to 3.25 percent, with many members highlighting the need for the OCR to rise back up towards neutral over time. Soft demand and the elevated unemployment rate were provided as reasons to be considered in the pace of tightening over the coming year.

Table 1 Participant comments

Participants’ comments are optional

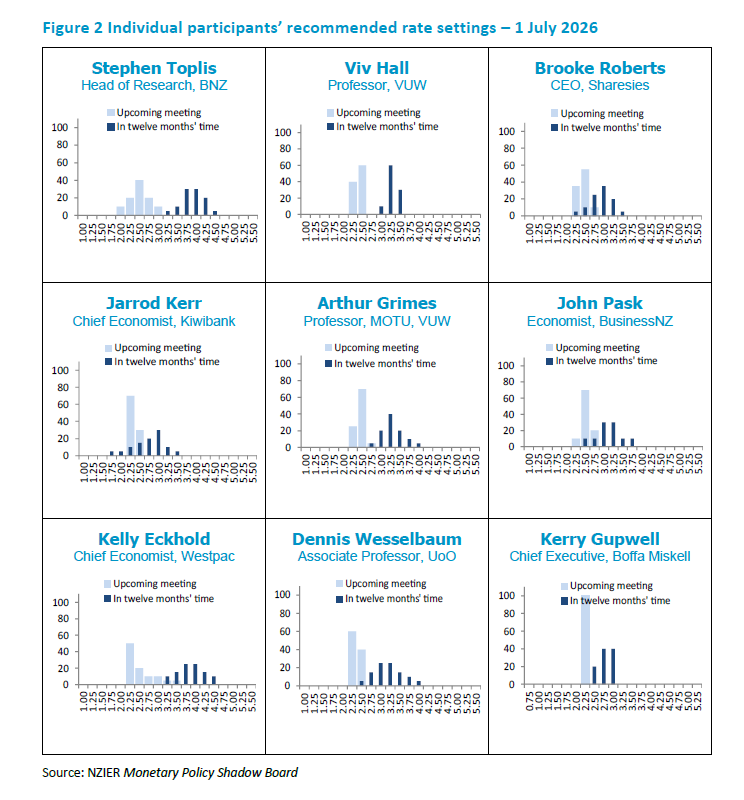

| Stephen Toplis | The RBNZ needs to ensure it is not adding to inflationary pressure at the moment. So, interest rates need to be raised towards neutral as soon as possible. Only when neutrality is achieved should it contemplate pausing. |

| Viv Hall | CPI and core inflation remain elevated relative to the 1-3% band. The OCR should therefore be increased to 2.50% at the upcoming meeting and subsequently moved progressively towards neutral. |

| Arthur Grimes | No comment. |

| John Pask | Inflationary pressures are likely to remain elevated for some time, despite the recent MOU between the US and Iran to stop hostilities for now. While the economy took a hit over the June quarter, it is appropriate that the RB starts the process of moving interest rates back up towards more neutral levels. |

| Jarrod Kerr | We’ve seen a supply shock, that now looks temporary. The oil price went up, demand was destroyed, and now the price has fallen back down. The impact on prices across the economy should be temporary as well. This is good news. Interest rates should be held to allow the economy to recover. There’s no need to jump at shadows. |

| Kelly Eckhold | The case for an eventually increasing OCR remains solid, but the urgency seems reduced given the marked reduction in energy prices. We need to see the June quarter CPI to assess the extent of the increase in core inflation. Revisiting in September looks like a sound approach. |

| Dennis Wesselbaum | Inflation seems to be peaking (GDPlive) while inflation expectations are still trending upward. On the real side, the Middle East Conflict seems to be cooling off, and oil and fertiliser prices recently fell substantially while global shipping costs are increasing again. Overall, GDP growth (GDPlive) remains subdued, such that keeping the rate stable one more time seems reasonable. |

| Kerry Gupwell | It's finely balanced, but I would prefer to hold at 2.25% in July. The case for tightening has strengthened, but I’d prefer one more round of data. Inflation risk is real, but activity and confidence still feel uneven, and the fuel shock may be easing. If wages, margins or expectations firm from here, I’d support a measured increase soon. |

| Brooke Roberts | Prices are rising faster than the Reserve Bank wants, mainly because of higher fuel costs. But with the economy still subdued and unemployment relatively high, there is no need for large interest rate increases. A 25-basis-point increase now, followed by gradual increases over the next year, strikes the right balance between controlling inflation and supporting the economy. |

About the NZIER Monetary Policy Shadow Board

NZIER’s Monetary Policy Shadow Board is independent of the Reserve Bank of New Zealand. Individuals’ views are their own, not those of their respective organisations. The next Shadow Board release will be on Monday, 31 August 2026, ahead of the RBNZ’s Monetary Policy Statement. Past releases are available from the NZIER website: www.nzier.org.nz.

Shadow Board participants put a percentage preference on each policy action. Combined, the average of these preferences forms a Shadow Board view ahead of each monetary policy decision.

The NZIER Monetary Policy Shadow Board aims to:

• encourage informed debate on each interest rate decision

• help inform how a Board structure might operate

• explore how Board members could use probabilities to express uncertainty.

For further information, please contact:

Ting Huang, Senior Economist

ting.huang@nzier.org.nz, 027 266 0969

Share this

Shadow Board recommends the Reserve Bank cut the OCR by 25 basis points in May

Shadow Board overwhelmingly in favour of keeping the OCR on hold in April