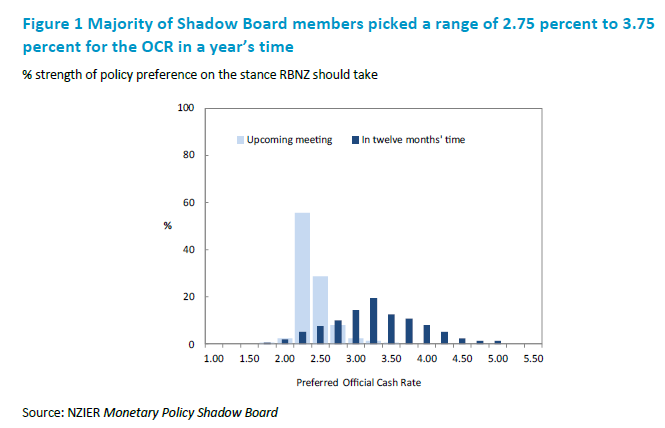

There is a split of views amongst the NZIER Monetary Shadow Board regarding the Official Cash Rate (OCR) at the upcoming May Monetary Policy Statement. The majority of Shadow Board members recommend the Reserve Bank of New Zealand (RBNZ) keep the OCR at 2.25 percent. They viewed that subdued growth and spare capacity in the New Zealand economy, along with the ongoing uncertainty over the impacts of the US-Israel war with Iran, justify keeping the OCR on hold in May. However, three members considered that the central bank should commence its tightening cycle with a small OCR increase now, given that the real interest rate has remained low for a prolonged period, which is adding to inflation pressures.

Regarding where the OCR should be in a year, Shadow Board members agree that the RBNZ should increase the OCR over the coming year. However, there is a range of views on the extent of OCR increases, with the majority picking a range of 2.75 percent to 3.75 percent for the OCR in a year’s time. Several members viewed that the RBNZ should raise the OCR as soon as possible, given the low real interest rate and the continued lift in inflation and inflation expectations. Other members are in favour of a more data-dependent approach to assess how the current fuel shock and spare capacity in the New Zealand economy balance out in terms of their implications for inflation and growth.

Table 1 Participant comments

Participants' comments are optional

| Stephen Toplis | The RBNZ has no choice but to tighten. The question is when. We think it should be moving interest rates to neutral as soon as possible. We also think it won’t. |

| Viv Hall | Headline CPI, non-tradable inflation, and 2-year ahead inflation expectations remain within or above the upper half of the 1-3% band, and some second-round inflation effects are already evident. But GDP growth is expected to remain subdued for the remainder of 2026. OCR should remain at 2.25% for this round, but should increase from July or September. Timing and extent will be data-depend |

| Arthur Grimes | The real OCR has been zero or negative for a prolonged period, contributing to inflationary pressures. It needs to rise over the next 12 months. While the current situation is highly uncertain, a (gradual) start to the tightening cycle should begin at this announcement. |

| John Pask | Inflation and inflationary expectations have moved up in light of the ongoing war in Iran, but at the same time both business and consumer confidence have taken a dive in light of continued uncertainty. The economy currently has spare capacity which suggests that the Reserve Bank should hold off raising rates for now until there is more clarity from forward looking data over coming weeks. |

| Jarrod Kerr | We hope that this supply-side shock will be short-lived. In the meantime, it is simply too early to assess the inflationary pulse, and the likely unwind. It is too early to gauge the impact on demand. And it is too early to see the adverse effects in the labour market. Therefore, it’s too early for the RBNZ to hike. If they do hike in July or September, they will be pre-empting inflation’s second round effects. Time will tell, and they have time to tell. |

| Kelly Eckhold | It’s become clear that interest rates need to rise in 2026. The current OCR was set assuming very different inflation conditions – specifically inflation close to 2% later in 2026. This is very unlikely now. An increase now is a down payment on returning the OCR to more neutral levels in the 3-3.5% range. We should not have such a low real interest rate for as long as delaying action would imply. |

| Dennis Wesselbaum | At this point, the situation in the Middle East is characterised more by “ambiguity” than “uncertainty.” In New Zealand, inflation expectations continue to drift higher, while inflation itself remains elevated and real economic activity appears to be gradually improving (GDPlive). With the effects of previous rate cuts still working through the economy, this is likely the last meeting at which holding the OCR unchanged can be justified. |

| Brooke Roberts | Hold the OCR at 2.25%. Current inflation pressure is coming from volatile oil prices and electricity prices, not domestic demand. With unemployment rising toward 5.6% and GDP growth at 0.2% last quarter, raising rates would tighten conditions unnecessarily. |

About the NZIER Monetary Policy Shadow Board

NZIER’s Monetary Policy Shadow Board is independent of the Reserve Bank of New Zealand. Individuals’ views are their own, not those of their respective organisations. The next Shadow Board release will be on Monday, 6 July 2026, ahead of the RBNZ’s Monetary Policy Review. Past releases are available from the NZIER website: www.nzier.org.nz.

Shadow Board participants put a percentage preference on each policy action. Combined, the average of these preferences forms a Shadow Board view ahead of each monetary policy decision.

The NZIER Monetary Policy Shadow Board aims to:

-

encourage informed debate on each interest rate decision

-

help inform how a Board structure might operate

-

explore how Board members could use probabilities to express uncertainty.

Ting Huang, Senior Economist

ting.huang@nzier.org.nz, 027 266 0969

Share this

Shadow Board recommends the Reserve Bank cut the OCR by 25 basis points in May

Line-ball call for keeping OCR unchanged in July, but the Shadow Board still sees higher interest rates as appropriate for the coming year